Estate planning for small business owners is critical, especially in California where the legal and financial landscapes are constantly evolving. This comprehensive guide, crafted for Shoup Legal, an esteemed estate planning law firm in Temecula, CA, aims to enlighten California business owners about the essential estate planning documents necessary to secure their business’s future. Each document will be discussed in detail, providing you with a clear understanding of its importance in the realm of estate planning.

The Will: Your Business’s Blueprint After Your Passing

Understanding the Role of a Last Will and Testament in Business Estate Planning

A will is the cornerstone of any estate plan. For business owners, it serves a dual purpose: managing personal assets and providing directives for the business after their death. In the will, you can specify who inherits your shares or interest in the business. This is crucial for sole proprietors and partners in small businesses, ensuring that your business legacy passes to the individuals you choose.

Crafting a Will: Considerations for Business Owners

When drafting a will, consider the future of your business. Do you wish to keep it within the family or sell it? Your will should reflect these intentions clearly to avoid any ambiguity. Additionally, it’s important to regularly update your will to reflect changes in the business structure or personal circumstances.

Trusts: An Essential Estate Planning Document for All California Estate Plans

How Trusts Benefit Business Owners

Trusts are powerful tools in estate planning, offering significant benefits for business owners. Firstly, they provide a level of control over how and when to distribute your assets, including business interests, are distributed after your death. This is especially important for ensuring that your business is passed on according to your specific wishes and timeline. For instance, you can stipulate that your beneficiaries receive their inheritance when they reach a certain age or meet specific conditions, ensuring they are ready to handle the responsibility. Knowing how a living trust works in California and understanding the necessity of having one is the first step.

Types of Trusts for Business Owners

Business owners can choose from several types of trusts, each tailored to specific needs and goals. A revocable living trust, for instance, allows you to maintain control over the trust assets (including your business) during your lifetime, with the flexibility to alter or revoke the trust as your circumstances change. On the other hand, an irrevocable trust, once established, cannot be easily changed but offers benefits like asset protection and tax advantages.

For those with family businesses, a family trust can be an excellent tool to ensure that the business remains within the family and is managed according to your wishes. Specialized trusts, such as an irrevocable life insurance trust (ILIT), can be used to hold life insurance policies, thereby excluding the death benefit from your taxable estate and providing liquidity for estate taxes and business expenses.

Avoiding the Probate Process in California

Probate is the legal process through which a deceased person’s will is validated, and their estate is distributed under court supervision. For business owners, having their business assets go through probate can be problematic for several reasons, so you’ll want to understand exactly how to avoid probate in California.

Firstly, probate is a public process. This means that the details of the estate, including business assets, become part of the public record. For a business, this can lead to unwanted public scrutiny and potentially reveal sensitive information such as the business’s valuation and ownership details. This exposure might not only affect the business’s competitive position but also impact the privacy and wishes of the family.

Secondly, probate can be time-consuming. The process can take anywhere from a few months to several years, depending on the complexity of the estate and the efficiency of the court system. During this period, the business assets are effectively in limbo, which can hamper the ongoing operations of the business. Decisions regarding management, investment, or distribution of these assets are stalled, potentially leading to lost business opportunities or decreased business value.

Finally, probate can be costly. There are court fees, legal fees, executor fees, and other costs associated with the probate process, which can significantly diminish the value of the estate, including the assets allocated for the business. These expenses are particularly concerning for smaller businesses, where the financial impact can be more pronounced.

Power of Attorney: A Critical Part of Every Estate Plan in California

The Role of a Financial Power of Attorney in the Estate Planning Process

In the realm of business, a Financial Power of Attorney (POA) plays a pivotal role in ensuring operational continuity, particularly during unexpected events such as an owner’s incapacity. This legal document enables a business owner to appoint a trusted individual, known as an agent or attorney-in-fact, to handle financial matters related to the business in their stead.

The importance of a POA in a business context cannot be overstated. In situations where the business owner is unable to make decisions due to illness, accident, or absence, the appointed agent can step in to manage business transactions, pay bills, handle payroll, negotiate and sign contracts, and make critical financial decisions. This ensures that the business operations continue seamlessly, preventing disruptions that could lead to financial losses or damage to the business’s reputation.

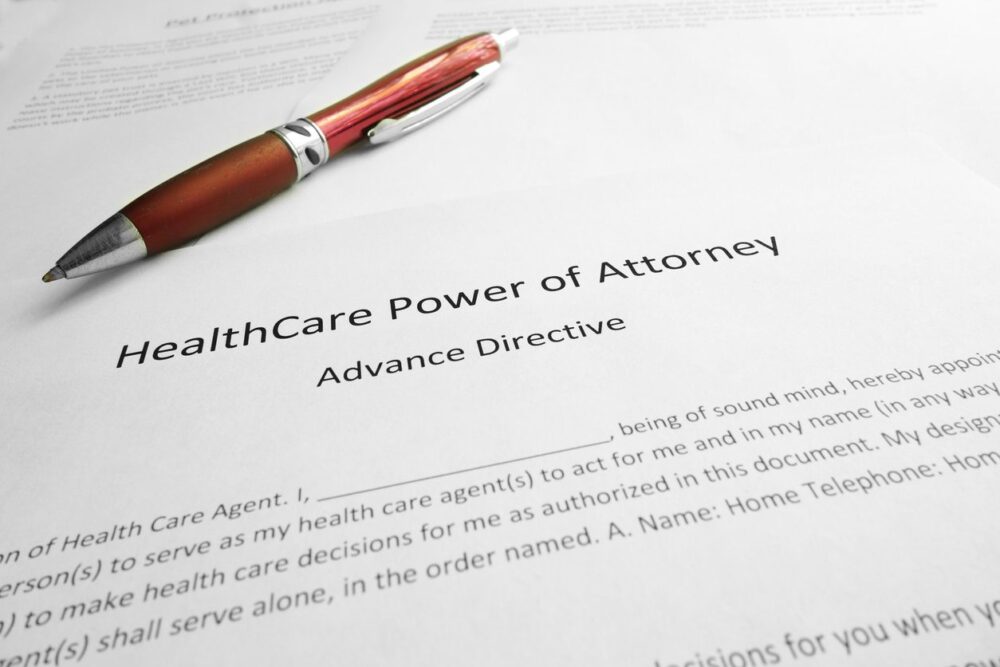

The Importance of a Medical Power of Attorney

In the realm of estate planning for business owners, much attention is given to the management and protection of assets. However, an equally critical component is the Medical Power of Attorney (POA), a document that addresses personal health decisions. This document should be drafted alongside an Advanced Healthcare Directive in order for business owners to designate a trusted individual to make healthcare decisions on their behalf if they become incapacitated or unable to communicate their wishes.

For business owners, the implications of a sudden health crisis can extend beyond personal concerns to impact the stability and continuity of their business. A medical crisis without a clear directive can lead to a situation where personal health decisions are delayed or mired in legal complications. This uncertainty can spill over into the business, causing operational disruptions, uncertainty among employees and partners, and potential financial instability.

A Medical POA ensures that there’s a designated decision-maker who understands your personal healthcare preferences and can make informed decisions swiftly. This can reduce the time spent in legal proceedings and minimize the impact on the business during a sensitive period. It also provides peace of mind to the business owner, knowing that both their personal welfare and business interests are being looked after. Learn more by reading “Do I Need a California Medical Power of Attorney?”

Choosing the Right Agent for Your Business

Choosing an agent for your Financial POA is a decision that requires careful consideration. The appointed individual should not only be trustworthy but also possess an understanding of your business operations and the acumen to make sound financial decisions. It’s often recommended to choose someone with a background in business or finance, and ideally, someone who is familiar with the inner workings of your particular business.

In some cases, business owners may opt to appoint a professional, such as an attorney or a financial advisor, as their agent. This can be particularly beneficial for businesses with complex structures or significant financial dealings. Professional agents can offer expertise and impartiality, ensuring decisions are made in the best interest of the business.

It’s also crucial to consider the scope of the powers granted in the POA. These can be broad or limited to specific types of decisions or transactions. For example, you might grant your agent authority to handle day-to-day transactions but reserve decisions about selling the business or large investments for yourself or a successor.

Buy-Sell Agreement: Planning for Future Changes

Importance of Buy-Sell Agreements in Business Succession

A buy-sell agreement is a must-have for businesses with multiple owners. It outlines what happens if an owner dies, becomes incapacitated, or wishes to leave the business. This agreement is crucial for preventing disputes and ensuring the business’s stability.

Crafting a Fair Buy-Sell Agreement

The agreement should detail how the business interest will be valued and who can buy an exiting owner’s share. It should also specify funding arrangements, like insurance policies, to buy out the owner’s interest. This document ensures that transitions are smooth and the business remains operational.

A Business Succession Plan: Mapping the Future of Your Business

Why Do You Need a Succession Plan?

Essential for Business Continuity and Legacy

A well-crafted succession plan is vital for ensuring the longevity and continued success of a business, especially when the owner steps down due to retirement, incapacitation, or death. This plan outlines a clear process for transferring leadership and ownership, and it is crucial for both small family businesses and large corporations. In fact, proper succession planning for family-owned businesses in California can often be the determining factor on whether or not the business survives following the death or incapacitation of the founder.

Addressing Key Business Continuity Concerns

The primary role of a succession plan is to address who will take over the business, how the transition will occur, and when it should happen. It should identify potential successors – whether they are family members, key employees, or external parties – and detail the training and development process to prepare them for their future roles. This preparation is crucial for minimizing disruptions during the transition period.

A comprehensive succession plan also addresses financial considerations, such as how the outgoing owner or their heirs will be compensated for their share of the business. This might involve buy-sell agreements, insurance policies, or other financial arrangements to ensure a smooth financial transition.

Mitigating Risks and Conflicts

Another critical aspect of succession planning is mitigating risks and potential conflicts that might arise during the transition. A well-thought-out plan considers various scenarios and includes dispute resolution mechanisms to handle disagreements among stakeholders. This proactive approach helps maintain harmony and stability within the business and the family (if it’s a family-run business).

Facilitating Strategic Growth and Adaptation

Beyond continuity and conflict resolution, succession planning plays a strategic role in the growth and adaptation of the business. By identifying and grooming successors, the business is prepared to evolve and adapt to changing market conditions and new leadership perspectives. This ensures that the business remains dynamic and competitive.

Legal and Tax Implications

Succession plans also involve navigating complex legal and tax implications. It’s important to structure the plan in a way that minimizes tax liabilities and aligns with legal requirements. This might involve working with estate planning attorneys, accountants, and financial advisors to develop tax-efficient strategies that comply with state and federal laws. Please refer to “How a Living Trust Can Reduce Estate Taxes” for additional information.

Personal and Emotional Dimensions

On a personal level, succession planning can be an emotional process, particularly for family-owned businesses. It involves conversations about retirement, legacy, and the future of the business. These discussions can be sensitive but are necessary for creating a plan that respects the founder’s vision and the aspirations of potential successors.

Developing a Comprehensive Succession Plan

Your succession plan should detail the process for transferring leadership and ownership. It should also include training programs for successors and contingency plans for unforeseen events. This plan is a roadmap for the future leaders of your business.

Selecting the Right Estate Planning Attorney

Understanding the Complexities of Estate Planning Laws in California

Choosing the right estate planning attorney is crucial for any business owner embarking on the journey of securing their business’s future. An experienced attorney doesn’t just draft documents; they provide invaluable guidance with the laws of your state, ensuring that every aspect of your estate and business planning aligns with your goals and complies with state laws.

The complexities of estate planning, especially when it involves business assets, require a specialized skill set. An attorney with expertise in business estate planning can navigate the nuances of estate taxes, business succession, trusts, and other essential elements unique to business owners. They understand the intricacies of how business structures impact estate planning and can offer solutions tailored to your specific situation.

For business owners in California, these estate planning documents form the backbone of a secure and prosperous future for your business. By understanding and implementing these essential documents, you can ensure that your business thrives and continues to serve your vision, even in your absence. Partnering with Shoup Legal, estate planning attorneys in Temecula and throughout Southern California, can provide the expertise and guidance necessary to navigate these complex legal waters, safeguarding the legacy of your business for generations to come.

What to Look for in an Estate Planning Lawyer

When selecting an estate planning attorney, consider their experience and specialization in business-related estate planning. Look for professionals who have a proven track record of working with business owners and who understand the dynamics of different business models, from sole proprietorships to large corporations.

Communication is key in any attorney-client relationship. Choose an attorney who listens to your concerns, communicates complex legal concepts clearly, and is responsive to your needs. They should be approachable and willing to work collaboratively with you and your other advisors, such as accountants and financial planners.

It’s also beneficial to choose an attorney who is well-versed in the latest laws and trends in estate planning and business law. Laws change, and strategies that were effective a few years ago might not be the best approach today. An attorney who stays updated and continues their education in estate planning can provide the most current and effective strategies.

Shoup Legal, a leading estate planning law firm in Temecula, CA, specializes in helping business owners throughout Southern California craft comprehensive estate plans. This guide serves as a starting point for understanding the critical documents needed for robust business estate planning. For more in-depth information and personalized guidance, Shoup Legal’s team of experienced attorneys is here to assist every step of the way.